Affiliate networks and publishers can face sign-off issues when finance, loans, credit or customer finance offers are involved.

An advertiser, lender, platform, principal firm or compliance team may ask for evidence before approving traffic. They may want to know whether the journey involves credit broking, whether FCA permissions are in place, whether financial promotions are approved, whether broker status is clear and whether customers understand what happens after submitting an enquiry.

These requests can feel frustrating if your business sees itself as a publisher or marketing partner rather than a credit broker. But if your content, forms or traffic sources introduce customers to lenders or finance providers, credit broking compliance may need to be considered.

This guide explains why sign-off issues happen and how affiliate networks and publishers can prepare.

Sign-off issues usually happen because finance-related traffic can create regulatory risk.

A lender, advertiser or platform may need to check:

If these questions are not answered clearly, sign-off may be delayed, refused or paused.

Affiliate networks and publishers often assume they are outside credit broking because they do not lend money.

That is not always enough.

Credit broking may be relevant where a business:

The FCA says firms wanting to engage in regulated activities as consumer credit brokers need authorisation.

For a broader explanation, read What Is Credit Broking? A UK Guide to Permissions, FCA Rules and the Right Route to Market.

Advertiser and platform sign-off issues often arise because the compliance position is unclear.

Common problems include:

Many of these issues can be fixed with better documentation, clearer wording and a stronger approval process.

Affiliate and publisher content may be a financial promotion if it promotes credit, credit broking or a customer finance journey.

This can include:

The FCA Handbook’s CONC 3 includes requirements for financial promotions and communications in relation to credit broking, including that communications should be clear, fair and not misleading.

For a practical guide, read How to Advertise as a Credit Broker Without Breaking FCA Rules.

Broker versus lender clarity is one of the most common sign-off issues.

The FCA says all credit brokers need to make clear in advertising that they are brokers and not lenders.

Affiliate and publisher pages can create risk if they use phrases such as:

Some phrases may be acceptable only if they are accurate, evidenced and properly qualified. Others may create a misleading impression if the journey is actually broker-led.

Customers should understand whether they are dealing with a publisher, affiliate, broker, lender or introducer.

For more detail, read Credit Broker vs Lender: Key Differences Explained.

Sign-off teams may ask whether the affiliate or publisher has FCA permissions or operates under another route.

Possible routes may include:

The correct position depends on what the business actually does.

An affiliate or publisher that only displays approved content may have a different risk profile from one that collects customer details, routes leads, creates finance comparison pages or controls the handoff to lenders.

For route options, read FCA Authorisation Routes for Credit Brokers: Direct Authorisation, AR and IAR Status.

Introducer Appointed Representative status may be relevant where an affiliate or publisher has a limited role in introducing customers or distributing approved financial promotions.

However, IAR status is narrower than full AR status.

An IAR should understand:

If the publisher or affiliate does more than simple introductions or approved promotional activity, IAR status may not be enough.

Advertisers and platforms often want to see the full customer journey, not just the landing page.

A useful customer journey map should show:

This helps sign-off teams understand what customers see, what they are told and where regulatory responsibilities sit.

For more on lead generation journeys, read Lead Generation in FCA-Compliant Credit Broking: What You Need to Know.

Affiliate and publisher models often involve collecting or passing customer data.

Sign-off teams may ask whether customers understand:

Consent and data sharing wording should match the real journey.

If a customer submits details on a publisher page and is contacted by another firm, the customer should not be surprised by that handoff.

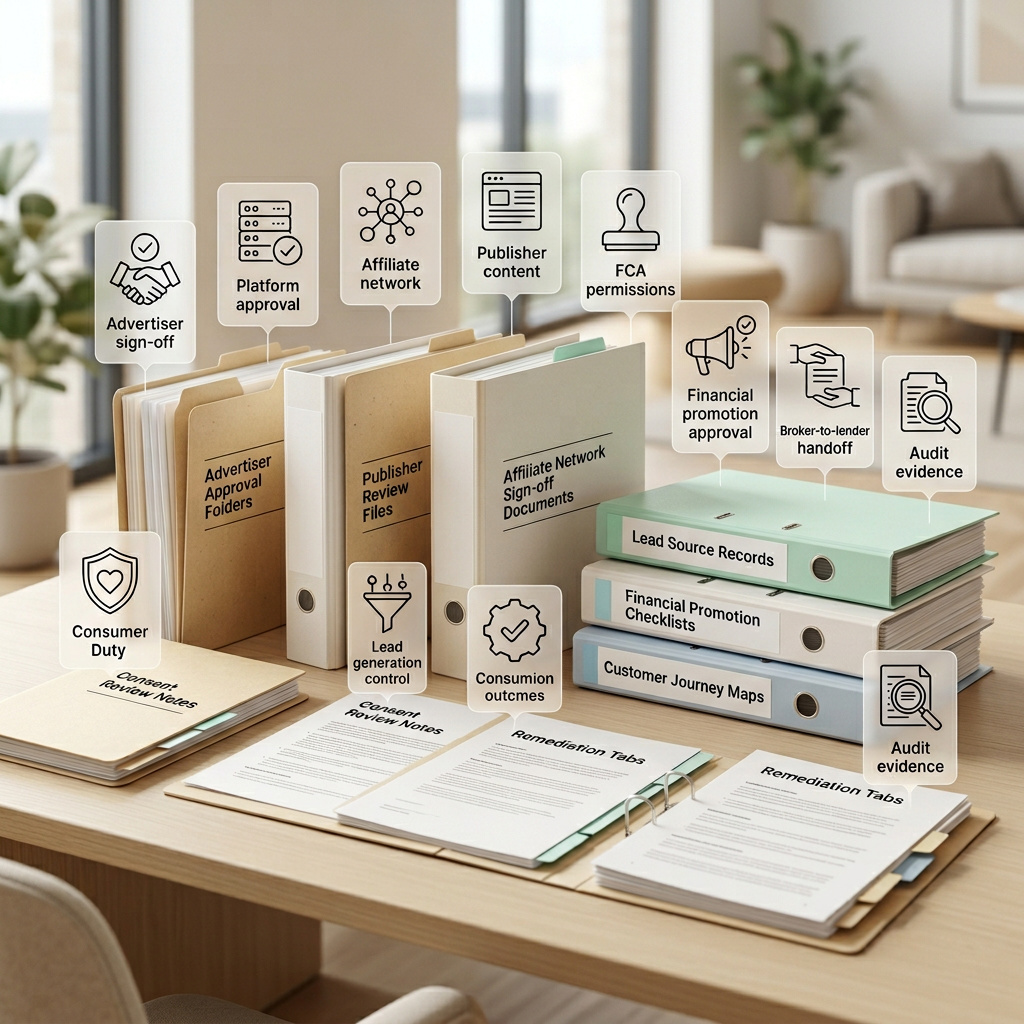

A strong sign-off pack should include evidence that promotions and pages have been reviewed.

Useful approval records may include:

If content changes after approval, there should be a process to review and reapprove it.

Advertisers and platforms may also want evidence that lead sources are monitored.

This may include:

This is especially important where an affiliate network manages multiple publishers or sub-affiliates.

Consumer Duty can affect affiliate and publisher journeys where retail customers are involved.

The question is whether the customer receives clear information and whether the journey avoids foreseeable harm.

Review whether:

For related guidance, read Understanding the Affordability and Suitability Rules in Credit Broking.

A sign-off request may ask for:

Having these documents ready can reduce delays.

A practical sign-off pack should include:

Common mistakes include:

For a broader mistakes guide, read The Biggest Mistakes Businesses Make When Understanding Credit Broking.

If sign-off is refused, do not simply resubmit the same content.

A practical response may include:

The goal is to identify the underlying issue, not just satisfy one checklist.

Authorised Compliance helps affiliate networks, publishers and finance lead generation businesses understand and control credit broking compliance risks.

Our support can include:

We help firms prepare clear, practical compliance evidence that supports advertiser, lender, platform and principal firm confidence.

You can read more in How Authorised Compliance Helps Credit Brokers Stay FCA-Compliant.

Yes. Affiliate networks may need to consider credit broking compliance if they help introduce customers to lenders, brokers or finance providers, or if they distribute credit-related financial promotions.

They may need a regulated route if their content or journey introduces customers to lenders, passes finance enquiries or promotes credit broking activity. The answer depends on the specific model.

Advertisers may ask for evidence to confirm that promotions, customer journeys, permissions, consent wording, lead sources and handoffs are controlled properly.

An Introducer Appointed Representative has a limited role, usually involving introductions or distributing approved financial promotions under a principal firm’s framework.

Where affiliate landing pages form part of a credit broking or finance journey, they should usually be reviewed and approved before use.

A sign-off pack should include regulatory route information, customer journey maps, approved promotions, screenshots, consent wording, lead source controls, complaints process and monitoring evidence.

The content should be reviewed again. Version control and live monitoring help make sure approved wording remains consistent after publication.

Yes. Authorised Compliance supports affiliate networks and publishers with credit broking activity reviews, financial promotion checks, customer journey mapping, sign-off packs, AR/IAR route assessment and ongoing compliance support.

Affiliate networks and publishers can play an important role in finance and credit broking journeys, but they need proper controls.

Advertiser and platform sign-off issues usually arise when the regulatory route, customer journey, financial promotion wording or lead source controls are unclear.

A strong compliance pack can reduce delays, improve partner confidence and make it easier to show that customers receive clear information before they are introduced to lenders or finance providers.

I’m Will Hurst, and I bring 20+ years of hands-on experience across credit broking, AR/IAR oversight, lender relationships and regulated finance operations.

Learn more about my practical, FCA-focused approach

Specialist compliance support for UK credit brokers, Appointed Representatives and Introducer Appointed Representatives. We help firms build practical, FCA-aligned compliance frameworks covering customer journeys, financial promotions, AR/IAR oversight, Consumer Duty, complaints, monitoring and regulatory applications.

Services

FCA application supportAR and IAR supportCredit broker complianceWebsite and financial promotion reviewsConsumer Duty supportCompliance monitoringComplaints and customer outcome reviewsRegulatory remediation supportUseful links

HomeCredit Broker ComplianceAR & IAR SupportInsightsContactPrivacy PolicyCookie PolicyComplaints ProcedureTerms of BusinessContact

Email: support@authorisedcompliance.com

Office address: Atlantic Business Centre, Atlantic Street, Broadheath, Altrincham, England, WA14 5NQ

Registered office: Atlantic Business Centre, Atlantic Street, Broadheath, Altrincham, England, WA14 5NQ

Authorised Compliance Ltd is a company incorporated in England and Wales with registered company number 15833435.

Authorised Compliance Ltd is authorised and regulated by the Financial Conduct Authority under Firm Reference Number 1025416.

Registered with the Information Commissioner’s Office under reference ZB802407.